Results 6,351 to 6,360 of 12096

Thread: Anandtech News

-

10-03-16, 01:03 PM #6351

Anandtech: The AnandTech Podcast: Episode 39

Here’s the second part of AnandTech’s smartphone podcast, post the Apple event where the iPhone 7 was launched. On the Podcast are Ian, Josh and Matt (apologies for his microphone) discussing a number of other devices and reviews that were launched around the same time as the iPhone. First up is a recap of Josh’s review of the Samsung Galaxy Note7, which has since been recalled due to issues with the battery - the team discusses some of the other features of the Note7 as well. Next is a discussion on the launch event of the Honor 8, a step up from previous Honor devices and uses HiSilicon’s top smartphone SoC, the Kirin 950, and also comes with dual cameras. Finally, the team covers the LG V20 smartphone launch, with the Josh having a good hands on with the dual display technology as well as some time on the new Android 7/N.

The AnandTech Podcast #39

Featuring- Dr Ian Cutress, Host, Senior Editor (@IanCutress)

- Joshua Ho, Senior Editor (@JoshuaHo96)

- Matt Humrick, Smartphone Editor, (@MattHumrick)

iTunes

RSS - mp3, m4a

Direct Links - mp3, m4a

Total Time: 1 hour 00 minutes 59 seconds

Outline hh:mm:ss

00:00 - Start

01:44 - Samsung Galaxy Note7

- 01:44 - Fires

- 03:11 - A week is not long enough for a full review

- 05:49 - Note7 Overview

- 07:06 - Snapdragon 820 (now) vs Snapdragon 821 (in future devices)

- 08:06 - Clarification on Google DayDream

- 09:03 - Specification Breakdown on Note7

- 10:03 - Why not Android 7?

- 11:08 - Discussing the Battery Issues

- 15:06 - Curved Displays

- 18:45 - Differences in Exynos 8890 vs Snapdragon 820

- 19:59 - Industrial Design

21:31 - Honor 8

- 21:31 - How Honor’s events differ to others

- 25:04 - Hardware

- 28:24 - EMUI

- 33:44 - Competition

- 34:07 - Color and Feel

- 35:59 - Honor vs Huawei (Nova and Nova Plus)

38:14 - LG V20

- 38:14 - Dual Screens

- 40:34 - Specifications, 3D NAND and Dual Cameras

- 45:19 - Android 7/Nougat

- 46:39 - Video/Audio Recording on V20

- 49:46 - ‘Quad DAC’

51:29 - LiveBlog Adventures (How we’re adjusting our LiveBlog process)

1:00:59 - FIN

Related Reading

The Samsung Galaxy Note7 (S820) Review

honor Press Event Live Blog

Hands On With the LG V20

Recent Podcasts

Episode 38 (9/16): Smartphones Anonymous (iPhone Launch)

Episode 37 (8/30): Intel's Developer Forum 2016 (Joule, Broxton, AMD Zen)

Episode 36 (2/29): Mobile World Congress 2016

Episode 35 (8/31): Windows 10 and Skylake Launch

Episode 34 (8/25): Interview with Dr. Genevieve Bell, Intel Fellow

More...

-

10-04-16, 08:19 AM #6352

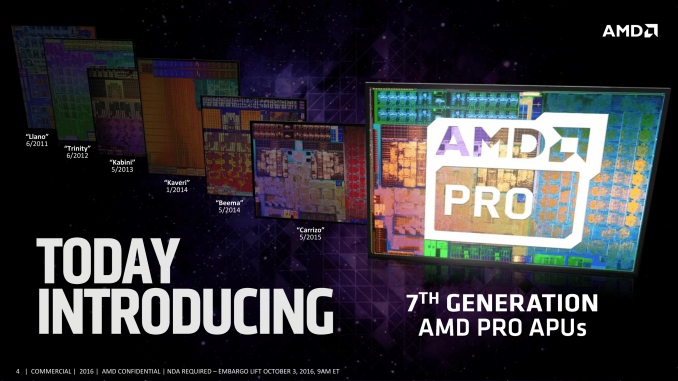

Anandtech: AMD Announces 7th Gen Bristol Ridge PRO APUs with Extended Support

There are a number of directions for ‘professional grade’ processors in the market, varying from embedded to long-life support to server functionality. AMD’s PRO lines of processors are akin to their consumer counterparts, except they run a guaranteed lifecycle of support with ‘image stability’ (guaranteed OS images) and extended OEM warranties. AMD’s PRO line typically covers both embedded systems via the BGA lower parts and commercial/enterprise systems with socketed units. This week AMD is announcing their PRO line using the latest AMD microarchitecture, Bristol Ridge, along with continued support for customer requested features.

If you’ve ever browsed for an OEM system, or in a brick-and-mortar shop, you may have come across a system labeled something along the lines of ‘PRO A8’ using an AMD APU. I recently wrote a small news piece which involved an HP system in my local store with a PRO name. These parts enable an OEM to build a particular system, either as a business-to-business sale or directly to customers, and guarantee a fixed longevity for replacements to that system. This is a requirement for a lot of government and business electronic installations – the ability to replace like-for-like in the event of failure. AMD states that the unit shipments of their PRO processor line for commercial, enterprise and the public sector has risen by 45% since mid-2014, or a 20.4% compound annual growth rate (CAGR).

The processors announced today are direct analogues of the consumer grade processors announced a couple of weeks ago, identical in specifications but with PRO in the name and a direct focus on support structures, management, virtualization, security and performance comparisons.

All these processors will support DDR4-2400 as standard, and offer USB 3.1 (10 Gbps) support via the appropriate chipset and Type-C with a re-driver chip to support reversible insertion (this is the same as the consumer platform). These new processors are all socketed parts designed for the AM4 platform for now, with BGA components likely to be declared later down the line.AMD 7th Generation Bristol Ridge PRO Processors Modules/

ThreadsL2 Cache CPU Base /

Turbo (MHz)GPU SPs GPU Base /

Turbo (MHz)TDP PRO A12-9800 2M / 4T 2 MB 3800 / 4200 512 800 / 1108 65W PRO A10-9700 2M / 4T 2 MB3500 / 3800 384 720 / 1029 65W PRO A8-9600 2M / 4T 2 MB3100 / 3400 384 655 / 900 65W PRO A6-9500 1M / 2T 1 MB 3500 / 3800 384 720 / 1029 65W PRO A12-9800E 2M / 4T 2 MB3100 / 3800 512 655 / 900 35W PRO A10-9700E 2M / 4T 2 MB3000 / 3500 384 600 / 847 35W PRO A6-9500E 1M / 2T 1 MB 3000 / 3400 256 576 / 800 35W

With the PRO APUs, AMD uses an ARM Cortex-A5 to implement ARM TrustZone, offering software agnostic (compared to Intel which does not) support for hardware-based security. This includes Secure Boot, Content Protection, per-Application security, fTPM 2.0, and support for Microsoft Device Guard, Windows Hello, independent fingerprint security, data protection and Bitlocker, among other things. AMD supports this via the DASH management protocol, which is ultimately CPU agnostic and allows users of other DASH systems to get up to speed.

AMD is positioning the APUs to be comparable to various Intel counterparts.

Performance-wise, for the launch, AMD states that in small form factors at 35W and mid-tier at 65W, performance compared to Intel is within 8% for the CPU, but AMD can offer +50-95% in graphics based or graphics accelerated workloads. In this case, AMD was positioning the PRO A12-9800E against the Core i5-6500T for the CPU comparison, and the PRO A10-9800 against the i5-6500 for the graphics comparison. We’ve asked to get these processors in for testing in order to compare.

The first systems using the new 7th Gen PRO APUs will be a set of HP Elitedesk 705 G3 systems, in Mini, SFF and mini-tower form factors. Due to the way these commercial systems are promoted, pricing and specifications will depend highly on the support contract aligned with the business customers. AMD is keen to point out that other customers will release their Bristol Ridge PRO based systems over the coming months.

Gallery: AMD Announces 7th Gen Bristol Ridge PRO APUs with Extended Support

More...

-

10-04-16, 09:22 AM #6353

Anandtech: One Month With: The Huawei TalkBand B3

I think I'm getting the reason why smartwatches exist now - or at least watches in general. When I was younger, before smartphones, I wore a simple cheap watch to tell the time. When smartphones came along, I ditched the watch as it was just 'another thing to carry', and its utility was superseded by the mobile phone. Having worn the TalkBand B2, and that space now being filled by the updated B3, I'm starting to get it. I think.

When I tested the TalkBand B2, a number of its features irritated me, such as the limited two-day battery life or the fact that the screen was incredibly bright at night, waking me up every time I turned over and the screen activated. The additional step counter, calorie burner and sleep monitor were interesting add-ons that provided a tale of being glued to my desk, or walking marathons during tech industry events, but these features have regressed in their utility over the initial fascination period. Now that I'm testing the B3, it's clear that there are some useful features for a watch that doesn't quite match the email facilities of a full Android Wear/Tizen device or an Apple equivalent, but it certainly gives more than a simple time telling mechanism.

Smartwatches (or semi-smart watches like the B3) are still new enough that I am continually asked what it is like, or how I feel it compares. There's a list of pros and cons, but I find that above basic clock face, it currently augments my life in two very specific ways.

Firstly, as an early morning alarm clock. On my wrist is a device on which you can set a time (via the app) and it will detect when I am sleeping in a low REM/light sleep up to 30 minutes before that set time and wake me by vibrating. This has a twofold advantage: I don't wake up from a deep sleep which would make me feel groggy due to the REM detection, and as a vibration rather than audio, my partner next to me is not woken up by any noise (unless I accidentally step on a cat / Lego making my way to the bathroom and produce four letter expletives). This benefit of a device like the B3 sounds like a minor plus, but it works wonders if the user has a set time to wake or has an early appointment to make. Unfortunately the Huawei app only has a limitation – it only lets the user set one such alarm time for that 30-minute wake-window, meaning that subsequent alarms are fixed at specific times in case you really want to snooze. It shouldn’t be too hard for the software developers to add in at least one more, for those that don’t have a regular sleep schedule.

Second, the TalkBand B3 augments my life as a Bluetooth headset. To clarify, with this watch you can take out the module with all the electronics (you need to do this to charge) while still leaving the strap on your wrist. As a Bluetooth headset, I can listen to music in one ear while keeping the other open for other noises (door bell, cat yowl, pasta boiling over) without the need for a wire or a dangling ear piece. While under the noise of cooking, I can listen to a YouTube clip, or take a meeting as the headset is very clear and easy to speak through. Perhaps this is just the utility of having a Bluetooth earpiece, as I lose the ability to tell the time when it's in use, but as part of my smartwatch I'm finding I use it almost every day in that headphone role. It also acts as a quick response if you are getting a call and your phone is in a bag/under some papers/under the cat. (Admittedly the B2 had a similar feature but I immediately disposed of the silicone insert for my ear within minutes of taking it out of the box, thinking it was just to protect the watch during shipping, but with the B3 I have found a large number of uses.) Using the B3 as an earpiece does drain the battery quicker, but only noticeably if it is constantly in use for several hours a day, and the heavier the music the more battery it consumes.

For users moving from the B2 to the B3, there are a few upsides and downsides with the transition. The big upside is battery life - I'm getting 3-4 days from the TalkBand B3, rather than the 18-24hr battery anxiety from the B2. With a longer battery life and my anecdotally good charge profile with a solid bump in charge with a quick ten minutes, I never feel that worried about the battery like I did with the previous generation. It sounds weird, but the joy of not worrying about charging the device is a positive and I'm sure that 3-4 days is well on its way to not having to worry about it in general. I don't think I could manage an every-day charging watch, especially one that I can't charge at night for the sleep monitoring/alarm.

One of the downsides is the evolution of the interface. Previously on the B2, some functionality was reserved for long-hold button presses, but now this has been moved to menus or options within menus. So what previously used to be a carousel of four five screens (time, steps, calories, sleep, workout) becomes several more (options, contacts) and if the user is relying on a wrist flick to activate the watch, the flick will iterate through them – but if the B3 decides to quickly skip the time (thinking it’s a double flick), it's a much longer process to get back to the time if the other hand isn't free (or you forget to swipe the other way). This could be mitigated by having the steps, calories and sleep data all up on display at once - there's a lot of wasted space having these three as separate items which could all be condensed into one screen.

Another downside, which has hit me later in testing the device, depends on how often the user wants to use the app. So, my anecdotal use case is that I rarely use the app anymore – the novelty of making sure I’ve slept enough and seeing the daily progression has lost its charm. But the other night, as I was getting into bed, I wanted to change the alarms on the watch. To do this it requires loading the app and making the adjustments. However, the Huawei Wear app has its own internal update system for software/firmware. It will not let you adjust anything without updating first, which is a slow five-minute process between the watch and the phone with two bright displays - when the immediate goal is just to go to sleep. Huawei needs to do one of a few things here - have a schedule to auto-update the firmware in the background after loading the app, and ensure the reboot the update requires doesn't cause the smart watch to vibrate. Or, auto-update the device after 5 minutes of charging. It's a small inconvenience, but when you really just want to go to sleep and change an alarm, it sticks out like a sore thumb.

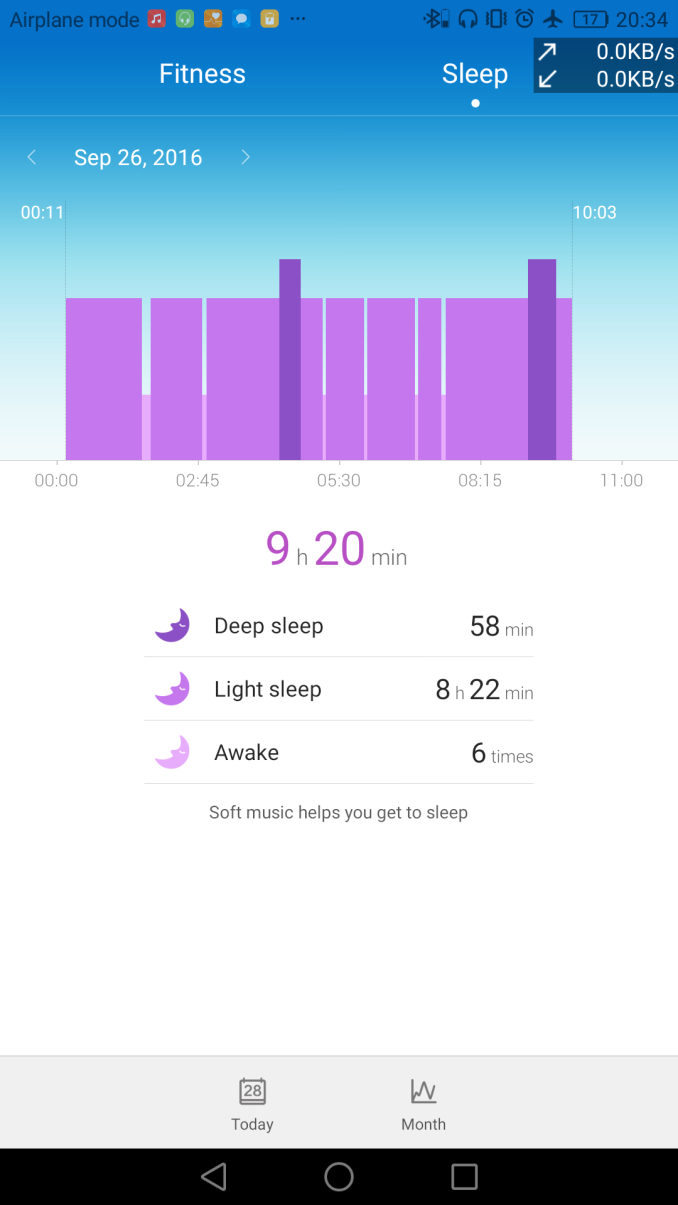

The software still remains a neutral point in the Huawei Wear ecosystem - it has gone through a few updates since our B2 experiential review, but it remains similar with steps and sleep with monthly or daily reports for viewing. Up until fairly recently, the software introduced a bug where daily step count profiles would not show for some reason, even though the data was there. That seems to be fixed now (sometimes it requires waiting 60 seconds), but ultimately Huawei does need to step up (pun intended) the potential data offering here. Being able to see per-day sleep cycles in a text format would be easier than the image below:

Also, some of Huawei's devices come with their own Health app which tracks steps for the user that carries the smartphone on them. The health app at least gives some indication that my 6867 steps so far today constitutes 374.2 kcal, equivalent to ~2.5 bowls of ice cream. That's the sort of tangential information which makes data gathering like this interesting, but here Huawei has two apps that don't talk to each other, with different features. I'd hazard a guess that this is a function of two separate software teams internally in different business units with little crossover.

The final point to discuss is the look. While the B3 looks refined, compared to the B2 it feels like a slight regression. The black plastic module is clearly a separate part of the housing, and creates a mismatch of aluminum and plastic with a large bezel on the screen. This is in contrast to the B2, which has a full unified metal body implementation, and blends seamlessly with the rest of the device. There are advantages to doing it the B3 way one would assume (cost comes to mind), but as an aesthetic package, I'd have to give the nod to the B2. I can confirm however that the B3 can take a trip through tomato sauce and still work after cleaning (it fell out of my ear at a hotel breakfast one morning). There's also a small minor thing of the strap that came with this unit: it's starting to already break away from the main metal housing:

Despite the issues, I'm finding myself using the B3 more and more as a personal alarm clock, a Bluetooth headset for meetings, and even as a one-eared headphone for music when I need to keep the other ear unobstructed. I'd love to see a light sensor and brightness toggle, preferably as a physical button, and a base camera that detects a face in front of it and turns on automatically. Whether these are possible with the same or better battery life would be interesting to see. The battery life is the biggest upgrade, and another successive jump in the same direction would be icing on the cake. The interface, while improved, still has issues and Huawei needs to integrate the various parts of the business in order to provide a unified user experience, especially if a user goes all-in with the brand. But I'm sitting here, writing this on an airplane, with music playing in one ear on a device that's easy to put away when needed. I'm certainly seeing the appeal of this sort of smartwatch.

Gallery: The Huawei TalkBand B3

The Huawei TalkBand B3 is currently listed over at Newegg, starting at $286 going up to $520. Compared to the Samsung Gear S2, which starts at $269, it's clear that Huawei is aiming for the same market but without the full-color display and an integrated experience, and instead is going for the Bluetooth headset angle for a similar price range.

More...

-

-

10-04-16, 04:05 PM #6355

Anandtech: Google Announces Pixel and Pixel XL Phones: Snapdragon 821, 5" & 5.5" Scre

At an event today in San Francisco, Google unveiled its latest vision for Android smartphones—the Google Pixel and Pixel XL. For this generation, Google nixes the familiar Nexus name, along with the cluttered and confused Nexus model numbering system, replacing it with the newer Pixel moniker and creating a unified hardware family that also includes the existing Chromebook Pixel notebook and Pixel C tablet.

Despite early rumors that Huawei would manufacture the new Pixel phones, that arrangement reportedly hit a snag and HTC eventually won the contract. Huawei partnered with Google for last year’s Nexus 6P (LG manufactured the Nexus 5X), and helped create a unique-looking, well-built phone with a few minor shortcomings. A follow-up device would be intriguing, but instead Google has come full-circle, enlisting the help of HTC who created the Nexus One, the very first Nexus phone.

Though make no mistake: Google may be contracting out the manufacturing, but all of the branding is explicitly Google. The name of the event "Made by Google" says it all. Google is presenting the Pixel as their phone, not an Android phone with stock firmware as how the Nexus was originally presented.

Google Pixel & Pixel XL

Overall Google is introducing two phones: the Pixel and the Pixel XL. The former is the successor to the Nexus 5X, while the XL replaces the Nexus 6P. Compared to past generations of the Nexus lineup and even competing phones, these two phones are much closer in construction and specifications. Other than their sizes, display resolution, price, and battery capacity, both phones have the same internals and configurations, including the same cameras with the same capabilities. As a result the Pixel XL is for all practical purposes a bigger Pixel, with a battery and display to match.

In terms of design and market positioning, one thing to note from the very start is that unlike the mid-range(ish) Nexus phones, the Pixel phones are meant to be flagship products. This means that Google is placing a greater focus on features and design, and that they’re also pricing the phones to match. So current Nexus users who are coming from $400 phones may be in for a bit of a shock at the $649+ Pixel. The Pixel may succeed the Nexus, but it is definitely not meant to be the Nexus.

The overall design for the Pixel then is another take on the rounded glass and aluminum designs we have seen in multiple phones over the years. The back of the phone uses both materials; the top-half (including the fingerprint sensor) is glass, while the bottom half is aluminum. Matt will have more on the feel in his hands-on, but at first glance it looks like it should be similar to other phones that have used this style. Meanwhile both phones will be available in a trio of colors. Taking a minor dig at Apple, Google has named these Quite Back, Very Silver, and Really Blue, with the latter being the pre-ordained “limited edition” color.

Meanwhile we’ll get to the hardware specifications in a moment, but it’s worth noting that Google is using the Pixel phones as a launch vehicle for a couple of their new technologies/initiatives. The Pixel is the first phone ready for Google’s Daydream VR platform, and pre-order customers will receive the associated Daydream View VR headset for free. The Daydream system wirelessly connects to the phone – so Google doesn’t need to worry about USB port alignments – and Google is ramping up the content side of the system with the usual mix of partnerships and leveraging YouTube’s growing capabilities.

The Pixel is also being used to launch Google’s enhanced Google Assistant functionality. The successor to the Ok Google functionality in previous generation phones, Google is further expanding what their voice-activated search and action software stack can do, with a focus on making that a core part of the Pixel phone experience. This also includes opening up the system to outside developers via a new SDK that will be launching next year, so that 3rd party developers can add actions to the system.

Under the hood, the Pixel phones pack a Snapdragon 821 SoC, which includes four of Qualcomm's custom 64-bit Kryo CPU cores. The two cores in the performance cluster have a peak frequency of 2.15GHz, while the other two cores in the power cluster have a peak frequency of 1.6GHz. Relative to the Snapdragon 808 and 810 SoCs found on the Nexus phones, this is a shift in both frequency and architecture. As Snapdragon 821 is just a new iteration of Snapdragon 820 there won’t be any surprises here, but based on what we’ve seen in other phones that have made a similar transition to 820, we should see a good performance uplift in both CPU and GPU tasks.Google Pixel Phones (2016) Google Pixel Google Pixel XL Google Nexus 5X Google Nexus 6P SoC Qualcomm Snapdragon 821

(MSM8996 Pro AB)

2x Kryo @ 2.15GHz

2x Kryo @ 1.6GHz

Adreno 530 @ 624MHzQualcomm Snapdragon 808

(MSM8992)

4x Cortex-A53 @ 1.44GHz

2x Cortex-A57 @ 1.82GHz

Adreno 418 @ 600MHzQualcomm Snapdragon 810 v2.1

(MSM8994)

4x Cortex-A53 @ 1.56GHz

4x Cortex-A57 @ 1.95GHz

Adreno 430 @ 600MHzDisplay 5.0-inch 1920x1080 AMOLED 5.5-inch 2560x1440 AMOLED 5.2-inch 1920x1080 IPS LCD 5.7-inch 2560x1440 SAMOLED Dimensions 143.8 x 69.5 x 8.5 mm 154.7 x 75.7 x 8.5 mm 147.0 x 72.6 x 7.9 mm

136 grams159.3 x 77.8 x 7.3 mm

178 gramsRAM 4GB LPDDR4 2GB LPDDR3 3GB LPDDR4 NAND 32GB / 128GB 16GB / 32GB (eMMC 5.0) 32GB / 64GB / 128GB (eMMC 5.0) Rear Camera 12.3MP Sony IMX378, 1.55µm pixels, f/2.0, PDAF + Laser AF, HDR+ 12.3MP, 1/2.3” Sony IMX377 Exmor R, 1.55µm pixels, f/2.0, Laser AF, Auto HDR, dual-tone LED flash 12.3MP, 1/2.3” Sony IMX377 Exmor R, 1.55µm pixels, f/2.0, Laser AF, Auto HDR, dual-tone LED flash Front Camera 8MP Sony IMX179, 1.4µm pixels, f/2.4 5MP, 1/4" OmniVision OV5693, 1.4μm pixels, f/2.0 8MP, 1/3.2" Sony IMX179 Exmor R, 1.4μm pixels, f/2.4 Modem Qualcomm X12 LTE (Integrated)

2G / 3G / 4G LTE (Category 11/9)Qualcomm X10 LTE (Integrated)

2G / 3G / 4G LTE (Category 6)Qualcomm X10 LTE (Integrated)

2G / 3G / 4G LTE (Category 9)SIM Size NanoSIM NanoSIM NanoSIM Battery 2770 mAh

non-replaceable3450 mAh

non-replaceable2700 mAh (10.3 Wh)

non-replaceable3450 mAh (13.18 Wh)

non-replaceableConnectivity USB 3.0 Type-C, 3.5mm headset USB 2.0 Type-C, 3.5mm headset USB 2.0 Type-C, 3.5mm headset Wireless 802.11a/b/g/n/ac 2x2 MU-MIMO, BT 4.2, NFC, GPS/GNSS 802.11a/b/g/n/ac 2x2 MU-MIMO, BT 4.2, NFC, GPS/GNSS 802.11a/b/g/n/ac 2x2 MU-MIMO, BT 4.2, NFC, GPS/GNSS Launch OS Android 7.1 Android 6.0 Android 6.0 Launch Price $649 / 749

32GB / 128GB$769 / $869

32GB / 128GB$379 / $429

16GB / 32GB$499 / $549 / $649

32GB / 64GB / 128 GB

The Pixel phones also include 4GB of LPDDR4 RAM, twice as much as the Nexus 5X, or 33% more than the Nexus 6P. Again this is pretty standard for Snapdragon 820 devices, and should provide a kick to multitasking performance under Android.

The amount of internal storage has also been significantly increased. The base models come with 32GB of NAND, while the high capacity models come with 128GB. Google has not officially disclosed which flash storage technology the Pixel is using, but it’s almost certainly UFS given the SoC and the phone’s flagship status. Like the previous generation Nexus phones, there’s no micro SD card support for the Pixel phones, so high NAND capacity is important. Coming off of the Nexus 6P little has changed – that phone was already available at 128GB – while this is a 2-4x capacity improvement over the more constrained Nexus 5X. Even then, Google is being mindful that 128GB is still a finite amount, and they will be offering unlimited photo and video storage in their cloud service for free in order to alleviate any capacity anxiety.

Helping to fill that capacity will be the phones’ camera. Here Google is using a 12.3MP Sony IMX378 sensor, which can capture 1080p video at up to 120fps, or 4K video at up to 30fps. Focusing the camera is provided by the usual combination of phase detection and laser detection. Meanwhile the front camera uses a smaller Sony IMX179, an 8MP sensor with slightly smaller pixels.

Somewhat surprisingly, there isn’t any OIS available on either phone. OIS is admittedly not very common on 5” and below phones, as the mechanism takes up space and Google wanted to avoid a camera hump. So the lack of OIS on even the Pixel XL may be a consequence of the shared camera model between the two phones.

That said, despite the lack of OIS, one of the major marketing points for the phone is its EIS image stabilization. Here Google claims they’re sampling the gyroscope at 200Hz in order to apply what they’re promoting as some of the best image stabilization on the market. So it will be interesting to see how well that holds up in practice. EIS has made great strides over the years, but OIS sets a very high bar in the flagship market.

Overall, Google spent a significant amount of time touting the image quality of the Pixel’s camera as a key product differentiator from both their earlier phones and the competition. Google’s partners used a very similar sensor on the last-generation Nexus phones, so it’ll be interesting to see just how things compare. Meanwhile on the software/implementation side, Google is also claiming that their capture time is faster than any other phone, including zero shutter lag in HDR+ mode.

Meanwhile, on the display side, the Pixel and Pixel XL use 5” and 5.5” AMOLED displays respectively. The smaller phone is a 1920x1080 display, while the larger phone bumps that up to 2560x1440. We’ll have a bit more here in our hands-on look at the phone, but in the meantime Google has somewhat frustratingly opted to define the color space in terms of NTSC. So from the specifications alone it’s not clear what these phones can do beyond the usual sRGB color space, though clearly Google is looking to offer some form of wide color gamut support. That said, as Google/HTC are sourcing panels from the usual vendors, it’s unlikely there’s anything here we haven’t seen before.

In terms of battery capacity, the smaller Pixel packs a 2770mAh battery – virtually identical to the Nexus 5X – while the Pixel XL bumps that up to 3450mAh, which is even more identical to the Nexus 6P. Google’s touting 26 hours of battery life for voice calls and 13 hours for internet browsing for the Pixel, and 32 hours/14 hours respectively for the Pixel XL. Both phones also implement USB Type-C quick charging, and Google says that the included 18W power adapter can fast charge the phone to “7 hours of use” in 15 minutes.

Moving on to the modem, both Pixels are relying on the Snapdragon 821’s integrated Qualcomm X12 LTE modem, which offers up to Cat 11 performance depending on the carrier. Interestingly, in their tech specs Google notes that there will be two configurations of the phone: a North American version, and a Rest of World version. The band support for the two phones is slightly different, and this likely has something to do with Google working with Verizon as their carrier partner for the US launch.

Wrapping up the specs, you’ll find the usual collection of wireless standards and interface ports. This includes 2x2 802.11ac WiFi, a USB Type-C port that supports 3.0 speeds, and a 3.5mm headset jack.

Pre-orders are starting today, with units available in stores (and pre-orders presumably arriving) on October 20th. Unlike the Nexus phones, Google is going head-first into the flagship market here, so the Pixels are priced accordingly. The 32GB Pixel is $649, and the 32GB Pixel XL is $769. Bumping the capacity up to 128GB will in turn add another $100 to those prices.

More...

-

10-04-16, 04:38 PM #6356

Anandtech: Google Announces Chromecast Ultra: 4K & HDR for Chromecast

Though the big Google news for today is of course the new lineup of Pixel phones, phones were only a small part of what Google had in store. Alongside their latest in mobile products, Google also used this morning’s event to announce the 3rd generation of Chromecast, the Chromecast Ultra.

The last Chromecast is more of a supplement than a replacement of the current Chromecast 2. Launching at $69, the Ultra’s major feature additions are 4K video support with HDR – essentially upgrading the Chromecast to keep up with the latest in video technology standards. Alongside the new hardware, Google has also announced that they are going to be upgrading their software ecosystem for 4K, including selling 4K movies through the Google Play store.

Unfortunately specifications on the hardware itself are limited at this time. Google isn’t saying much beyond the fact that the Ultra is capable of decoding and displaying 4K content. From the hardware capabilities alone it’s clear that the underlying SoC is something capable of decoding 4K content and outputting it over HDMI 2.0 with HDCP. This should, with any luck, also mean that we’re finally getting a Chromecast from Google that can handle 1080p60, which has been the Achilles Heel of the prior versions of the media streamer. Given that it’s a Google product, I’d also expect that VP9 support is present, while HEVC support is going to be more questionable.Google Chromecast Family Chromecast Ultra Chromecast (2) Chromecast Audio Processor ? Marvell ARMADA 1500 Mini Plus SoC (88DE3006) Marvell ARMADA 1500 Mini Plus SoC (88DE3006) Memory ? 512MB N/A Wireless 1x2 2.4GHz/5GHz 802.11ac 1x2 2.4GHz/5GHz 802.11ac 1x2 2.4GHz/5GHz 802.11ac Display Output 4K w/HDR

(HDR10 & Dolby Vision)1080p N/A Max Video Decode 4K 1080p30 N/A Ports HDMI 2.0

Micro-USB

Ethernet (On Power Adapter)HDMI 1.3

Micro-USB (Power)3.5mm Combo Jack

(Analog + Optical Audio)

Micro-USB (Power)Launch Date 11/2015 09/29/2015 09/29/2015 Launch Price $69 $35 $35

On the video format front, the big news here of course is that the Chromecast Ultra can handle 4K video. However Google didn’t stop there; the Ultra also supports HDR video via both the HDR10 and Dolby Vision standards. The latter is a particularly interesting development, as to date Dolby Vision support has been very rare. I’m very curious to see where Dolby Vision factors into Google’s larger plans given that they’re bucking the trend here and have their own major content distribution platform. At least for owners of TVs that support he standard, this could help kickstart its use in streaming services.

Meanwhile as Google opted to spend the bulk of their efforts on updating the internals of the Chromecast, the overall design has not significantly changed since last year’s Chomecast 2. The Ultra is still a puck – albeit one that looks slightly thicker than the last – and implements a pair of antennas for improved WiFi reception. At the same time, for users and environments who can’t make WiFi work for them, Google has added Ethernet capabilities to the Ultra by placing an Ethernet port on the power adapter, giving users a wired option to fallback to.

Wrapping things up, the Chromecast Ultra will be launching in November for $69. At almost double the price of the Chromecast 2, this is not going to be replacing the cheaper Chromecast, but instead serve as a premium option for 4K. At the same time, as one of the original Chromecast’s primarily selling points was its low price, it will be interesting to see how the Chromecast Ultra does now that it’s priced closer to stand-alone media streamers. For 4K this is still very much a budget option, but it’s not going to fit the impulse purchase market like the Chromecast 2 does.

More...

-

10-05-16, 03:18 AM #6357

Anandtech: Hands On With the New Google Pixel Phones

After Google’s launch event today in San Francisco, I had an opportunity to get my hands on its new Pixel and Pixel XL phones. My initial impression is that they are decent-looking, well-made phones. Google took a more active role in creating these phones than previous Nexus devices, taking the lead not just in hardware selection, but design as well. Using quality displays and not having a camera bump on the back were decisions driven by Google, for example.

The phones share the same design and internal hardware, so my observations apply to both the Pixel and Pixel XL. The aluminum chassis has a sandblasted finish and rounded corners that do not dig into the palm. The back has a distinctive design, with glass covering the top third. This functions as an RF window for the various antennas, but its size seems more cosmetic. I would prefer more aluminum on the back, both for aesthetic and durability reasons, but the partial glass back does help the Pixel stand out from other aluminum phones. The recessed fingerprint sensor sits within the glass region and is easy to locate. The rear camera, dual-color LED flash, laser autofocus module, and a noise cancelling microphone are lined up in the top-left corner similar to the iPhone. The Pixel’s camera, however, sits flush with the back and is covered by the rear glass.

The front is edge-to-edge glass and nondescript. The upper and lower bezels are needlessly large, and there’s a lot of wasted space in the lower bezel, which does nothing but serve as a place to rest your thumb. Instead of using the space for capacitive buttons, or just making the bezel smaller, Google commits two fouls by making the bezel large and then using onscreen navigation buttons. The upper bezel is sized to match, with another curious design choice. The Pixel’s ambient light and proximity sensors are located below the earpiece instead of next to it. It’s possible the large upper bezel is necessary to fit the rear camera above the screen, which is necessary to avoid a camera bulge, but we will not know for sure until we see a teardown.

With so much room above and below the display, front-facing stereo speakers would have been nice. Instead, there’s only a single downward-firing speaker. While there are two symmetric grilles flanking the centered USB Type-C port, the second covers only a microphone. At least there’s still a 3.5mm headphone jack located on the top edge. The SIM tray slides into the left side, and both the nicely-textured power button and single-piece volume rocker are on the right side. One thing that really bothers me about the Nexus 6P is the button placement; every time I touch it I inadvertently press the power button, turning it on when I want it to stay turned off or vice versa. The button placement is better with the Pixel phones, with the power button closer to the top, so this should be less of an issue now.

The edges are rounded on the back, eliminating another pressure point, and chamfered on the front, the only place we see a hint of HTC 10 styling. The sides are still flat, which makes it easier to hang on to than an iPhone, but not quite as comfortable.

I did not have too much time to play with the Pixel’s camera, but its autofocus worked quickly and accurately within the confines of the demo room, even when I covered the laser module. The rear camera includes 1080p30, 1080p60, and 4K video recording modes, along with 120fps slow-motion video at 1080p and 240fps at 720p. Electronic image stabilization (EIS) for video recording (the camera still does not have OIS) was one of the highlight features mentioned in Google’s presentation. While testing the camera, I noticed that EIS is used for video modes up to 1080p60 but not when shooting 4K video. There’s still a processing/power hurdle to clear.

I also spoke with Qualcomm and learned that Google optimized its HDR+ algorithm to run on Snapdragon 821’s Hexagon 680 DSP, taking advantage of vector instructions to enable HDR processing with zero shutter lag. Qualcomm also said this approach consumes less power than running the algorithm on the CPU.

The Pixel phones also use Qualcomm's Aqstic audio codec that's capable of 192kHz/24bit playback, but does not use Qualcomm's Quick Charge 3.0 technology. Instead, it adheres to the USB Power Delivery specification, delivering up to 18W of power.

Both Pixels use wide-color gamut AMOLED displays, with Google claiming 100% NTSC coverage. Unfortunately, while poking around in the display settings panel, I did not see any options to adjust white point or change the display to sRGB mode. It's possible this option is hidden again in the developer settings.

With prices starting at $649 for the 32GB, 5-inch version, Google is positioning its Pixel phones to compete with Apple’s and Samsung's flagships. This will no doubt disappoint Nexus fans who were hoping for a more affordable option. It's also a questionable strategy, considering the lack of brand awareness around Nexus/Pixel among the general public and Google's lack of retail exposure. Its alignment with Verizon should help, but I imagine it will be difficult to convince someone looking to buy an iPhone or Galaxy phone to buy a Pixel instead, especially when its premiere feature, the one advantage it has over every other Android phone, is timely software and security updates—not exactly a sexy selling point. For those who do value up-to-date software, and who do not want to tinker with custom ROMs, the new Pixel phones are the new price of admission.

More...

-

10-05-16, 07:39 AM #6358

Anandtech: Zotac ZBOX CI523 nano Fanless Skylake-U mini-PC Review

Passively cooled computing systems are popular amongst consumers worried about noise from fans and their associated maintenance requirements (particularly, for industrial use-cases). Traditionally, fanless high-performance PCs have come with a high price tag. However, with the focus on low-power Core-series CPUs by Intel, we have many vendors targeting this market segment with affordable models. Zotac started a new lineup of passively cooled ultra-compact form factor (UCFF) machines in the C-series back in mid-2014. Initially, the members of the series utilized either Atom-class or -Y series CPUs (with a sub-10W TDP). With Skylake, Zotac has re-engineered the design to accommodate 15W Skylake-U CPUs. Today, we are taking a look at the Zotac ZBOX CI523 nano, a passively-cooled alternative to the Intel Skylake NUC NUC6i3SYH.

More...

-

10-05-16, 09:38 AM #6359

Anandtech: CEATIC 2016: Sharp Showcases 27-inch 8K 120Hz IGZO Monitor with HDR, also

While we’re not CEATIC, a Japanese technology show, news has come via PC Watch regarding a new publicly announced milestone in monitor production. For any journalist that has attended either IFA, Computex, CES or MWC over the past year, it would be hard going to miss one of the super large (80-inch plus) 8K monitors doing the rounds. While highly impressive in their own right, current 8K displays on show typically have a low pixel-per-inch value in order to achieve a good panel off the production line. So despite the fact we can get 4K panels on smartphones (Sony Xperia Z5 Premium is 4K in 5.5-inch, or 806 PPI), expanding the size at that pixel density is difficult with panel yields. Also, moving 8K down to a 'monitor size' has been hidden at the panel companies internal research divisions until now.

So this is where the Sharp monitor on display at CEATIC gets interesting. The IGZO display is down at 27-inches, marking a 326 PPI, just hitting at the door of large FHD smartphone displays. The panel is also listed at 1000 nit brightness. But to double down on specifications, the stand listed the display as supporting 120 Hz while in 8K mode, and also supporting High Dynamic Range, or HDR. This requires a large amount of data to be pumped into the display, and as a result a photograph of the rear shows eight separate DisplayPort cables being used in order to give the display the data it needs. 8K120 with HDR is no easy task, suggesting 7680x4320 at 10 bits per color channel (so 30-bit for RGB) at 120 times a second would suggest needing 120 gigabits per second of bandwidth at a minimum (or 15 GB/sec). That's even before you discuss overhead, which will push that higher.

Needless to say, this is a prototype panel. Businesses with large enough checkbooks are free to try and estimate a figure for such a display, because it will be a while before a device of these specifications hits commercial availability.

Also in the display was a 2.87-inch display, offering 1920x2160 resolution and rolling in at over 1000 pixels per inch (1008 PPI). This was described as ‘4K to both eyes’, affording a combined display suitable for head-mounted units or virtual reality headsets. Compare this to the HTC Vive, which uses a 1200x1080 screen per eye at 3.62 inches per panel, making it 447 PPI. This gives the Sharp panel a specification of over double the amount of pixels in a given area. Of course, with that comes cost and the ability to feed that display with enough data either over cable or other means. Still, it’s an interesting prospect.

More...

-

10-05-16, 10:45 AM #6360

Anandtech: Market Trends Q2 2016: SSD Shipments Up 41.2% YoY, PC Sales Up on Q1

Sales of SSDs in the first quarter of 2016 were up 41.2% year-over-year, based on findings from TrendFocus*, a storage market tracking company. Shipments of all types of SSDs, including drives for client and server systems, were up sequentially and year-over-year, which again proves that NAND-based storage devices are taking the place of traditional hard drives both inside client PCs and enterprise machines.

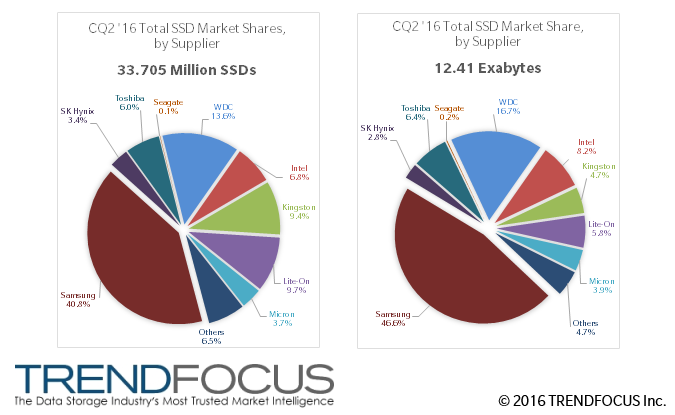

SSD Sales now above 33.7 Million Units

Shipments of SSDs in the second quarter hit 33.705 million units, which is nearly 10 million units higher than in the same period a year ago and up 9.5% from the previous quarter, according to TrendFocus. According to IDC and Gartner, sales of PCs were also relatively strong in Q2 compared to Q1: the industry sold 62.4-64.3m units, which is flat or slightly up (depending on who you take numbers from). Meanwhile, the SSD market for client PCs and servers has been growing rapidly for many quarters, therefore, and all-time high shipment units in Q2 came as no surprise.

There are multiple industrial trends that help to accelerate adoption of SSDs by both client PCs as well as servers:SSD Market at Glance in Q2 2016

Data by TrendFocus

All numbers are millions of units, Exabytes or GigabytesForm-Factor

(Units)Interface

(Units)Total Average

CapacityDrives

2.5"/3.5"Modules

mSATA/M.2SATA SAS PCIe Units Exabytes Client 16.637 13.0 ? ? ? 29.637 8.24 278 GB Enterprise 3.868 0.2 3.2 0.668 0.2 4.068 4.17 1025 GB Total 20.505 13.2 3.2 0.668 0.2 33.705 12.41 368 GB

Firstly, price. Entry-level SSDs are getting cheaper thanks to rapid per-GB price declines of TLC and 3D TLC NAND flash memory. This is combined through competition among vendors as well as the adoption of multiple module form-factors. In the second quarter, average contract prices of 128 and 256 GB SSDs dropped to $37.20 and $60.80 per unit, respectively, according to DRAMeXchange. For example, 120/128 GB SSDs for $35-$38 are easy to find at Amazon. Moreover, there are plenty of drives with 240 GB or 256 GB capacities that cost less than $60 at Amazon.

Secondly, rapid performance improvements brought by NVMe protocol and new controllers supporting PCIe 3.0 bus stimulate strong demand for newer SSDs by enthusiasts and boutique PC makers.

Thirdly, new technologies (3D NAND, stacking, etc.) enable companies like Samsung and Toshiba to build SSDs that challenge HDDs not only in terms of performance but also in terms of capacities, thus stimulating demand from datacenters.

Average SSD Capacity Hits 368 GB

The total capacity of all SSDs sold in the second quarter achieved 12.47 Exabytes, up 93% year-over-year and 24.1% quarter-over-quarter, based on estimations from TrendFocus. The company believes that the whole industry produced 29 EB of NAND flash (up 17% sequentially) and SSDs consumed 42.5% of that output. The major increase of NAND flash bit supply was driven by the ramp up of 3D NAND and TLC NAND memory by leading manufacturers. This is due to the growing demand for non-volatile storage from many applications and industries. While this fast growth of NAND supply looks impressive, several industry insiders are indicating that demand is outpacing supply, which would drive up prices. However larger chips help mitigate this issue, keeping cost/GB down.

Meanwhile, the average capacity of an SSD, combining consumer and enterprise, increased such that:

- 325 GB to 368 GB from Q1 2016 (a 13.2% QoQ growth) and,

- 268 GB to 368 GB from Q2 2015 (a 37.3% YoY growth)

The recent declines of NAND flash memory pricing made SSDs with 240/256 GB and higher capacities considerably more popular than they were a year ago in the PC segment, driving average client SSD capacity to 278 GB. Moreover, companies like Samsung and Toshiba introduced enterprise-class SSDs that can store 8 TB or even 15 TB of data, which helped average capacity of a datacenter-class SSD to increase to just over 1 TB for the first time in Q2 2016.

Strong demand for high-capacity datacenter-class SSDs in the recent quarters, as well as shift for high-end models, has helped a number of companies increase the average SSD capacity per unit of their sales significantly in the second quarter both sequentially and year-over-year (the combination of HGST and SanDisk shipments under Western Digital brand somewhat distorts the picture, but it still is in line with general trends). Meanwhile, short supply of NAND and focus on unit sales triggered declines of average SSD capacities for companies like Kingston, Lite-On and some others.Average Capacities of SSDs by Top Manufacturers in Q2 2016

Data by TrendFocusQ2 2016

(av GB per unit)Q1 2016

(av GB per unit)Q2 2015

(av GB per unit)Intel 445.4 288.0 331.6 Kingston 183.0 185.3 141.2 Lite-On 220.2 229.2 255.3 Micron 384.0 398.6 396.8 Samsung 420.4 360.2 283.3 SanDisk/Western Digital 452.0 227.4 243.2 SK Hynix 304.3 231.5 231.9 Toshiba 391.1 282.4 252.7 Others 264.8 281.2 164.6 Overall 368.2 GB/unit 324.9 GB/unit 268.2 GB/unit

Samsung Retains Leadership Amid Slight Drop of Unit Sales

Samsung controlled about 36.3% of the global NAND flash production in Q2 2016 based on revenue, according to DRAMeXchange. Moreover, its NAND bit shipments were up 15% sequentially, the same company reports. Nonetheless, when it comes to SSDs, the quarter was a mixed bag for the company.

Sales of Samsung SSDs in Q2 totaled 13.75 million units, up from 10.45 million in the same period a year before (an increase of 31.5%), but slightly down from 14.16 million units in Q1 (a decrease of 2.9%). Meanwhile, the total capacity of Samsung’s SSDs in the second quarter increased to 5.78 EB, up from 2.96 EB in Q2 2015 (up 51.2%, slower than the industry) and 5.1 EB in Q1 2016 (+12%, slower than the industry).

Due to a slight drop in unit sales, Samsung’s market share decreased to 40.2%. While the company is still well ahead of everyone else, its SSD unit shipments and market share have been decreasing for two straight quarters now. The reasons for that are more or less clear: the company is gradually increasing average capacities of its SSDs, boosting their average selling prices (average capacity of a Samsung SSD in Q2 was 420 GB), but the amount of NAND flash it can use for SSDs seems to be somewhat limited (we will discuss this issue below). As a result, Samsung focuses on more lucrative high-capacity drives, sacrificing market share and unit shipments for higher per-unit selling prices.

Western Digital’s SanDisk retained #2 position in the SSD market for Q2: it shipped 4.58 million drives (up 106% YoY and 6.2% QoQ) and increased its market share to 13.6% in Q2 2016. What is even more important is that the company doubled the amount of NAND flash memory it used for its SSDs from the previous quarter (2.07 EB vs 0.98 EB) and nearly quadrupled it from the same period a year ago (0.54 EB). The average capacity of a SanDisk SSD in the second quarter was 452 GB, according to TrendFocus, the highest in the industry. Despite the fact that SanDisk lost a part of its OEM SSD business lately, its performance on the SSD market in the recent quarters was rather impressive.

Important notice: When analyzing historical data for SanDisk, keep in mind that starting from the second quarter of 2016 sales of SanDisk and HGST are combined under the Western Digital name. HGST does not sell a lot of drives (in 1H 2015 it controlled roughly 1.0%-2.6% of the global SSD market, so its shipments were 200-600 thousand units per quarter at best), but it sells a lot of high-end high-capacity SAS SSDs. Therefore, the addition of HGST’s product mix to SanDisk’s has a strong impact on average SSD capacities of Western Digital.

Lite-On, which sells SSDs under Lite-On and Plextor trademarks, maintained its third place in the rankings of SSD makers with 9.7% market share, based on data from TrendFocus. The company sold 3.27 million drives (up 131% YoY, but down 14.9% QoQ) with a total capacity of 0.72 EB (up 100% YoY, but down 19% QoQ). Since Lite-On only serves the client PC market, the average capacity of its SSDs was 220 GB, down both sequentially and year-over-year. This happened because in the recent quarters Lite-On introduced a number of inexpensive drives (particularly, under its Plextor brand), which attracted consumers with budget constraints that typically focus on smaller drives anyway. One of the reasons why Lite-On released such Plextor drives was timing (the M8Pe-series high-end SSDs are hitting the market only now), but another was the short supply of NAND in general. As a result, the company managed to increase its unit sales, but at the cost of average capacities and ASPs.

Kingston managed to boost its SSD shipments slightly to 3.17 million units (up 24.3% YoY and 1.2% QoQ) in the second quarter and increased its market share to 9.4%. Its total data (exabyte) shipments remained flat sequentially but are +61% compared to the same period a year ago. Since Kingston serves the entry-level segment of the client PC market, the average capacity of its SSDs is among the lowest in the industry at ~183 GB.

Intel’s positions as a supplier of SSDs has not been particularly strong in recent quarters, but in Q2 2016 the company managed to increase sales of its SSDs to 2.29 million units (up 18.6% YoY and 83% QoQ) and overtook Micron and Toshiba. The total capacity of Intel’s SSDs shipped in the second quarter was around 1.02 EB, a 59% growth over the same period a year ago and 183% more than in the previous quarter. The average capacity of an Intel SSD also increased to 445 GB, which signals that the company was particularly successful with its high-capacity enterprise-class drives introduced in April.

Toshiba also managed to amplify shipments of its SSDs in Q2 2016. The company sold 2.02 million drives (up 122% YoY and 54.2% QoQ) and its Exabyte shipments totaled 0.79 EB (up 243.4% YoY and 113.5% QoQ). Toshiba’s average SSD capacity also increased significantly compared to previous quarters. Keep in mind that Toshiba supplies NAND memory to Phison (who sells it with its controllers) as well as to companies like Lite-On. Therefore, despite the relatively small market share (6%), Toshiba is not an underdog when it comes to SSDs.

Micron and SK Hynix, who both the other NAND flash producing fabs, commanded 3.7% and 3.4% of the SSD market in Q2 2016 with shipments of 1.25 and 1.15 million units respectively. Micron has a strategy to become a vertically integrated maker of NAND-based devices and it expects sales of own-brand SSDs to get higher over time.

Client SSDs: Modules Are Gaining Momentum

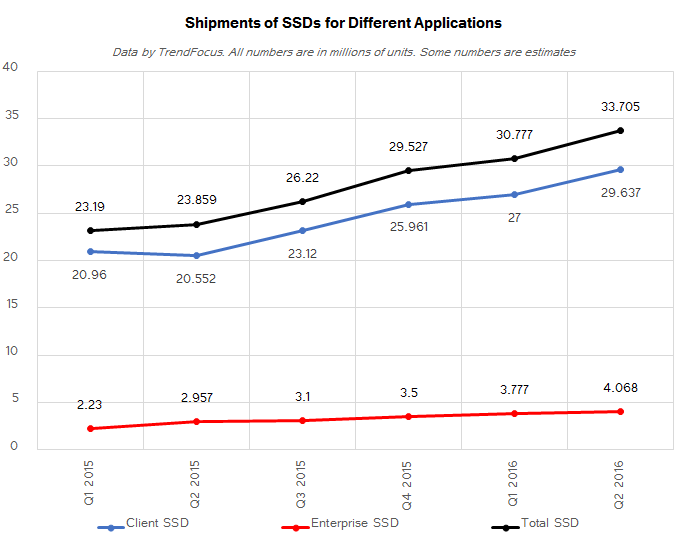

Of the 33.7 million SSDs that various manufacturers shipped in Q1 2016, roughly 29.6 million of the solid-state drives sold were aimed at client PCs, compared to ~4 million were designed for servers. Sales of SSDs in the PC space increased 44% year-over-year, outpacing general market trends. The total available market of enterprise-grade SSDs hit 4.068 million units and grew healthy 37% YoY.

When it comes to SSDs for client computers, it is noteworthy that modules are gaining traction. In Q2, approximately 13 million of SSDs in M.2 or mSATA form factors were shipped, TrendFocus estimates. Growing popularity of SSD modules is conditioned by increasing market share of ultra-thin laptops (which modern 2.5-inch HDDs are reducing in importance) and adoption of PCIe-based drives by higher-end models. Shipments of solid-state drives in module form-factors are still behind sales of SSDs in traditional drive form-factors (i.e., M.2/ vs. 2.5”/7 mm), such that ~13 million M.2/mSATA units compared to 16.637 million units. Nonetheless, as PC form factors continue to shrink and performance of mainstream SSDs is getting higher, it is expected that modules with a PCIe interface will become more widespread in the client PCs. Some people even say that next year PCIe/NVMe SSDs in M.2 form-factor will go beyond module sales for 2.5” drives with a SATA interface.

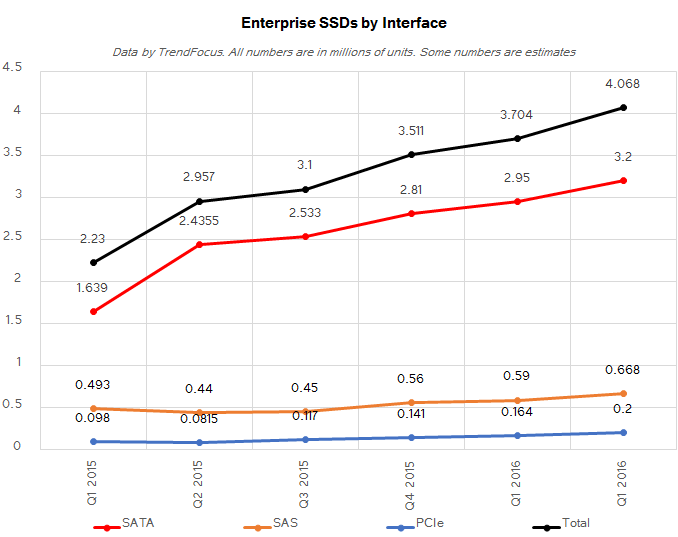

Enterprise SSDs: SATA Is Still King of the Hill

Various data centers across the globe continued to replace their 10K/15K HDDs for mission-critical applications with SAS or even PCIe SSDs in the second quarter of the year. To hit performance targets (both in terms of IOPS and bandwidth), operators of data centers do not need a lot of such drives, which is why cumulative shipments of SAS and PCIe SSDs only hit ~870 thousand of units (668K SAS, 200K PCIe) in the aforementioned period. By contrast, with 3.2 million units shipped, SSDs with SATA interface remained the choice for the majority of enterprises.

TrendFocus believes that they key suppliers of enterprise-grade SSDs are Samsung, Intel and Western Digital (HGST). All three companies increased average capacities of their SSDs quite tangibly during the quarter, which may be an indicator that sales of their server drives were on rather high levels.

Demand for SSDs Poised to Rise, But Supply of NAND Remains Major Concern

Solid-state drives are becoming more widespread these days and in many cases they capture market share from traditional hard drives. The current demand for SSDs is healthy and shipments are growing, but there is a great concern about supply of NAND flash memory for SSDs. In fact, there are several factors which limit the amount of NAND flash memory available for solid-state drives:

- The evolution of planar NAND has stalled at 14 nm or 16 nm nodes and we are hardly going to see any newly designed 2D NAND ICs suitable for SSDs. Manufacturers are not going to build new fabs to produce 2D NAND. Without geometry scaling and new production facilities, supply of 2D NAND will not grow. In fact, companies like Samsung are already mulling about cutting-down 2D capacities, thus reducing supply. There are talks about planar QLC NAND memory, however the feasibility of this technology is currently limited, with manufacturers discussing 'write once, ready many' applications only at this time.

- 3D NAND yields and manufacturing volumes are gradually improving. In the meantime, demand for non-volatile memory is skyrocketing.

- NAND flash makers have long-term supply agreements with large smartphone vendors (Apple, Samsung, etc.), who recently increased storage capacities of their flagship devices. Hence, manufacturers have to meet demand from such partners first.

- China-based makers of smartphones now install 64 or 128 GB of NAND flash into their handsets and someone has to supply them the memory. Companies like Huawei, Oppo, Nubia and others sell hundreds of millions of smartphones every quarter and the amount of NAND they consume is gargantuan.

Some readers will notice that both production and consumption-related factors have already impacted Samsung. The company was the first to stop expanding its planar NAND manufacturing facilities and the first to start high-volume shipments of 3D NAND. At present, the company’s SSD sales are growing slower than the market due to tight supply of NAND. Other makers are barely expanding 2D production and yet have to transit to 3D NAND. As a result, we would not expect them to improve their output of flash memory significantly in the coming quarters.

The exponential growth of the demand for NAND flash memory amid a linear growth of its supply will ultimately have an impact on NAND and SSD pricing (the pace of depreciation of prices, to be precise). As a result, per-GB prices of SSDs may remain at the current levels for quite some time. In the coming months we are going to find out how stable pricing environment affects demand for SSDs.

*Please note that the numbers mentioned in this news story were determined from a combination of press releases and previous announcements from TrendFocus, or estimates based on previously released numbers and relationships by the company. If you need precise numbers for business decisions, you should acquire the full report from TrendFocus.

Recent Storage Reviews

The Toshiba OCZ VX500 Review: 256GB, 512GB and 1024GB

The Samsung 850 EVO Review: 4TB

Evaluating the Toshiba OCZ RD400 M.2 Drive on a Skylake NUC

The Intel 540s Review: 480GB

The Crucial MX300 Review: 750GB

More...

Quote

QuoteThread Information

Users Browsing this Thread

There are currently 13 users browsing this thread. (0 members and 13 guests)

Bookmarks